Single Audit Rules Clarified for Provider Relief Fund Recipients

The U.S. Department of Health and Human Services (HHS) recently clarified rules for single audits of nonfederal entities that received pandemic-related assistance from the Provider Relief Fund (PRF).

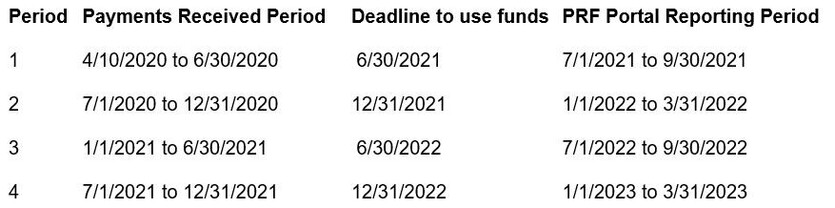

HHS updated its PRF FAQs to state that the reporting in the PRF Reporting Portal will be based on when PRF payments were received, and that PRF recipients must only use payments for eligible expenses, including services rendered and lost revenues during the period of availability, as outlined in the following table:

The updated FAQs also state that nonfederal entities will include PRF expenditures and/or lost revenues in the schedule of expenditures for federal awards (SEFA) for fiscal years ending on or after June 30, 2021. The AICPA Governmental Audit Quality Center (GAQC) confirmed with HHS that the new guidance supersedes previous guidance indicating PRF reporting was to begin for fiscal years ending Dec. 31, 2020, and later.

The FAQs also clarify that a nonfederal entity's SEFA reporting is linked to its report submissions to the PRF Reporting Portal. For a fiscal year end of June 30, 2021, and through fiscal year ends of Dec. 30, 2021, recipients are to report on the SEFA the total expenditures and/or lost revenues from the Period 1 report to the portal. For a fiscal year end of Dec. 31, 2021, and through fiscal year ends of June 29, 2022, recipients are to report on the SEFA the total expenditures and/or lost revenues from the Period 1 and Period 2 reports to the portal. For fiscal year ends on or after June 30, 2022, SEFA reporting guidance for Period 3 and Period 4 will be provided at a later date.

The GAQC stated that it expects the 2021 Compliance Supplement to advise that because the PRF report is to be tested as part of the reporting type of compliance requirement, auditors should think about delaying the start of the compliance audit of the PRF program until recipients have completed the PRF report.

For more information, visit the GAQC website.