New Lease Accounting Standard Update and Its Effect on Financial Reporting

By Mark G. McCarthy, Ph.D., CPA, and Douglas K. Schneider, Ph.D., CPA

Lease transactions have been engaged in by corporations for decades. As with other issues in financial reporting, accounting rule makers have desired to provide useful information about leasing in the financial statements. In February 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2016-02, which led to the creation of a new accounting standard for leases, Accounting Standards Codification (ASC) 842. This new accounting standard supersedes ASC 840, the previous standard for leases, and requires the capitalization of operating leases as a “right-of-use” asset as well as recognizing a lease obligation for the same amount.

Lease Accounting’s Previous Rules

Prior to ASC 842, any lease classified as an operating lease only required disclosure in the notes to the financial statements. This was originally governed by Statement of Financial Accounting Standards (SFAS) No. 13, Accounting for Leases, which was issued by the FASB in November 1976. When the FASB instituted the Accounting Standards Codification in 2009, the lease standard was classified as ASC 840.

Under SFAS No. 13 and, subsequently, ASC 840, if a company was able to structure a transaction that did not meet any of the four requirements1 to be considered a capital lease, it was considered an operating lease, and no asset or long-term liability was reported on the balance sheet. A company could sign a 10-year lease for $100,000 per year, and if it qualified as an operating lease, there was no recognition of a liability or an asset. The only item recognized in the financial statements was the $100,000-per-year lease or rent expense on the income statement. The total expense related to the lease over the 10-year period was one million dollars, 10 payments of $100,000. In the notes to the financial statements, the company was required to disclose that it was obligated to pay $100,000 per year for the next five years, and then the remaining total was simply reported as amounts owed “thereafter.”

The same company could enter into a different transaction with $100,000 yearly payments for 10 years, and if one of the four criteria for capital lease classification was satisfied, the transaction with the same payments for the same period of time would be capitalized, and a liability would be recognized for the present value of the lease payments. Between the depreciation of the leased asset and interest expense on the lease liability, total expense over the 10-year period amounted to one million dollars, the same as the operating lease. To avoid the issue of having to classify a transaction as a capital lease, in many cases companies would intentionally structure the lease contract so that none of the four criteria were met.

The previous lease standard allowed for what is referred to as “off-balance sheet financing.” This is where the company using the asset essentially has complete control over its use and access to all of its benefits but does not have to report in the balance sheet the amount owed to have that control and benefit. For example, in the Delta Air Lines 2017 annual report, disclosure Note 7, the company reported leases of aircraft, airport terminals, maintenance facilities and several other types of assets. The total future minimum lease payment reported by Delta amounted to $16.2 billion. In the balance sheet, Delta reported $20.8 billion in noncurrent liabilities. If the present value of the $16.2 billion in operating lease payments are assumed to be $10.3 billion and were reported on the balance sheet, Delta’s noncurrent liabilities would increase by 50% from $20.8 billion to $31.1 billion. In addition, Delta’s total assets would increase by almost 20%.

A New Rule Is Issued

When ASU No. 2016-02 was issued, it was clear that numerous companies were going to be affected by the new standard. However, net income reported on the income statement was essentially going to remain the same under the new standard. Stipulated by the new accounting rule, the combination of interest expense on the lease liability and amortization expense on the “right-of-use” asset are to equal the amount of the operating lease payment. For example, if a company was making a $100,000-per-year lease payment, under the previous standard, the yearly lease expense reported was $100,000. The journal entry to record the payment is:

Lease expense………………………………….. 100,000

Cash……………………………………. 100,000

Under the new standard, with the same $100,000 payment, if interest expense for the year on the lease liability is assumed to be $30,000, then amortization of the “right-of-use” asset is required to be $70,000 ($100,000 payment - $30,000 interest expense) so that the sum of the two amounts equals the lease payment of $100,000. The journal entry to record the lease payment is:

Interest expense……………………………….. 30,000

Lease liability…………………………………. 70,000

Cash…………………………………… 100,000

Then the amortization of the “right-of-use” leased asset must be recognized. The journal entry to record this item is:

Amortization expense……………………….. 70,000

Right-of-use asset…………………… 70,000

In the financial statements, the combination of the $30,000 in interest expense and $70,000 of amortization is reported as a single amount of lease expense for $100,000. Under both the old and new rules, the total lease expense for the year is $100,000. In subsequent periods, the amount of interest expense will be less each year due to the decline in the lease liability balance, and the amortization of the right-of-use asset will increase, so the two amounts always combine for a $100,000 total.

The Balance Sheet Impact of ASC 842

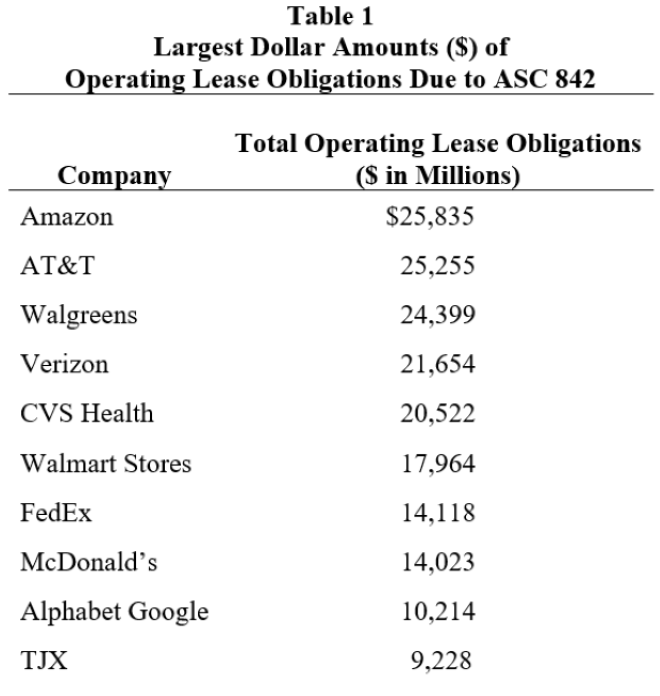

The significant effect of ASC 842 was the new recognition of a liability as well as an asset. Table 1 presents a list of selected Fortune 500 companies with some of the greatest dollar amount of operating leases reported as liabilities in the first year the firm adopted ASC 842.

The amounts presented in Table 1 show the gross dollar amounts for each company of the change due to the new accounting standard, but it does not show the materiality the new standard has on some of the largest companies’ financial ratios. AT&T was one of the companies with the largest amount of new operating lease liabilities. In its Dec. 31, 2019, annual report, AT&T reported $25.3 billion in new operating lease liabilities and $349.7 billion in total liabilities. The additional lease liability only represented 7.23% of AT&T’s total liabilities. For Dollar General, another Fortune 500 company but not one of the companies with the large dollar amount of new reported lease obligations, its $8.8 billion increase due to operating leases represents 54.5% of the $16.1 billion in total liabilities reported in its Jan. 31, 2020, financial statements.

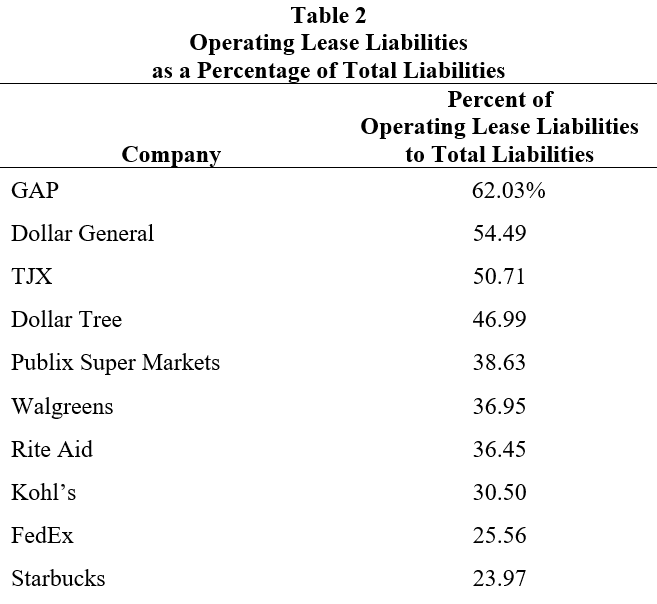

Table 2 presents the companies in which the additional liability created by ASC 842 had the greatest impact on total liabilities. In addition to the material effect on Dollar General’s total liabilities, the new accounting standard caused GAP’s and TJX’s total liabilities to more than double, with the operating lease liabilities accounting for more than half of the total liabilities. Fortune 500 companies not substantially affected by ASC 842 include General Electric, Exxon Mobil, Apple and IBM, where the additional liabilities amount to less than 5% of total liabilities in the year of adoption.

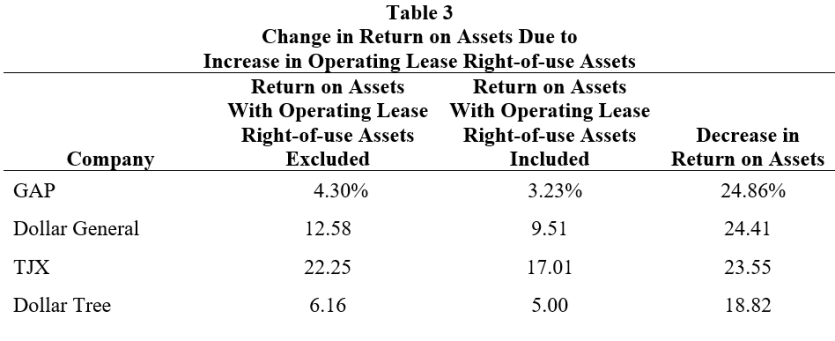

Different ratios are used to evaluate a company’s profitability. A common ratio employed is return on assets, which measures how well or efficiently a company is using the assets provided by creditors and stockholders. The ratio is calculated as net income divided by average total assets. Table 3 presents the companies in which the return on assets ratio was affected the most due to the capitalization of the right-of-use operating lease assets.

Not unexpectedly, the four firms having the largest percentage decrease in return on assets are the same four companies in which the increase in liabilities due to the implementation of ASU No. 2016-02 was the largest. The return-on-assets ratio for GAP of 3.23%, which included the right-of-use assets in total assets, was 24.86% lower than return on assets under the previous accounting standard, where operating leases were not capitalized as part of total assets. Other companies that experienced a significant decline in the return-on-assets ratio are Dollar General, TJX and Dollar Tree.

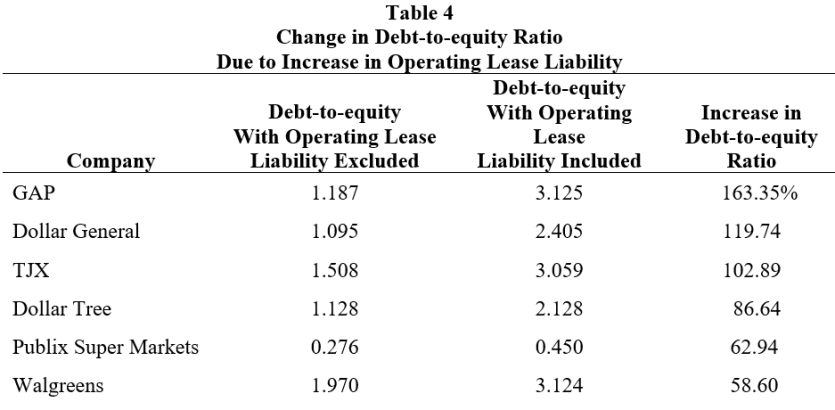

One measure of risk used by analysts when evaluating a company is the debt-to-equity ratio, which is calculated as total liabilities divided by total equity. The higher the value, the riskier the company. ASC 842 added liabilities to any company involved in what previously was classified as an operating lease and reported in the notes to the financial statements. Table 4 presents the six companies whose debit-to-equity ratio was affected the most.

The companies with the four largest increases in the debt-to-equity ratio, GAP, Dollar General, TJX and Dollar Tree, are the same four with the decrease in return on assets from Table 3. In addition, the next two companies whose debt-to-equity ratio was affected the most by ASC 842 are Publix Super Markets, with an increase from 0.276 to 0.450, or a 62.94% increase, and Walgreens, with a 58.6% increase in the ratio from 1.970 to 3.124. Other large companies with at least a 30% increase in their debt-to-equity ratio are Kohl’s, FedEx and Best Buy.

The goal of financial reporting is to provide useful information to decision makers. The FASB is continually evaluating current accounting standards and looking for ways to improve the information provided in the financial statements. In 2016, the FASB decided that it was more useful to provide operating lease amounts on the balance sheet instead of in the notes to the financial statements. With the issuance of ASC 842, companies must report a “right-of-use” asset and operating lease liability in the balance sheet for the present value of the future cash outflows from the lease payments. This standard does not affect or change the net income reported. Under the new standard, what is reported as lease expense, interest on the lease liability and amortization of the “right-of-use” asset is equal to the lease payment, the same amount that was reported as lease expense under the previous standard.

While the new standard does not affect the reported earnings of the lessee, amounts and ratios derived from the balance sheet have changed materially for some companies. When analyzing a company and comparing ratio values under the new accounting standard, users of the financial statements should be aware of changes in the ratios due to the change in the accounting standard.

FOOTNOTES

1. Capital lease tests:

a. Title transfers to lessee and end of lease.

b. Lease agreement includes a bargain purchase option the lessee is expected to exercise.

c. The present value of the minimum lease payments is greater than or equal to 90% of the fair value of the leased asset.

d. The lease term is 75% or more of the useful life of the leased asset.